Cash Stash: Standby for Emergencies

This post may contain affiliate links. We may earn a commission if you purchase via our links. See the disclosure page for more info.

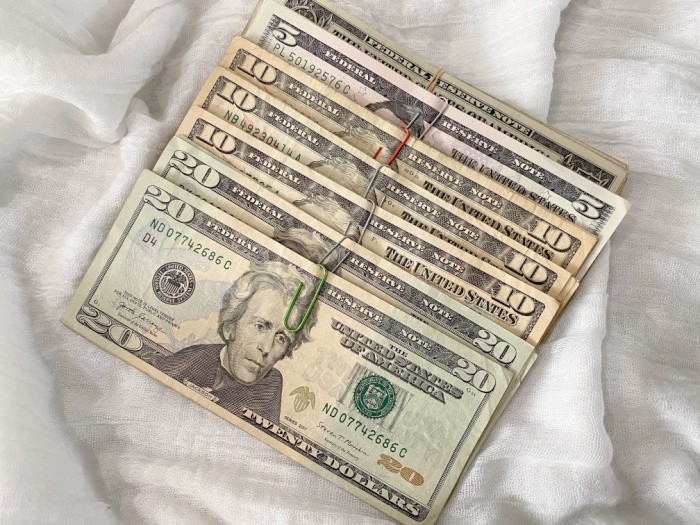

Are you prepared for a financial emergency that might be the result of a natural disaster, job loss, accident, or injury? Having cash on hand is an important part of any household budget. It’s essential to have an emergency fund separate from everyday spending money and bills.

But how much cash do you need to have available? Let’s look at why having cash on hand is important and what factors to consider when creating your emergency fund. I’m no financial professional, but financial experts have a lot to say about having a certain amount of cash on hand!

Cash Stash: Standby for Emergencies

Why You Need to Have Cash on Hand for Emergencies

Having cash on hand is an essential part of any financial planning. It’s important to have a separate emergency fund so that unexpected expenses or other financial setbacks won’t wreak havoc on your budget. But exactly how much cash should you have available? In this blog post, we’ll explore why having cash on hand is important and what factors to consider when determining the size of your emergency fund.

The Benefits of Having Cash On Hand

When it comes to preparing for a financial emergency, the most obvious item to include in the plan is having cash or liquid assets available. This provides flexibility since it can be used to pay bills or make needed purchases. What you don’t want is to find yourself needing to wait for credit approval or needing access to a bank account. It allows you to avoid taking out high-interest loans if there’s an unexpected expense like a car repair.

When you have enough cash on hand, you don’t have to worry about unexpected events. Not every place is still accepting cash, but if they are, you’ll have it on hand! A stash of emergency cash is SMART! 10 Ways to Save Money Using Cash

It makes sense to have most of your funds safely deposited in a bank or credit union. Those deposits are like “cash” since they are considered pretty liquid if held in a checking account or savings account. The challenge is, in many emergencies, the banks are also closed, so access to your emergency funds may be limited. Having cash reserves in denominations that will be accepted at most all establishments can make things easier.

How Much Should You Have Stashed Away?

Experts suggest having at least three months’ worth of income saved up as an emergency fund. Hopefully, the cash savings to cover those three months of expenses is enough money to cover the expected bills. Be proactive in your plans so sudden expenses are covered without dipping into savings or using credit cards. For those who are self-employed, six months’ income is suggested since income may not be as steady as salaried employees.

It’s also important to factor in other sources of income when calculating your emergency funds such as investments, side hustles, inheritance, etc. This will allow you more wiggle room if you experience an unplanned but necessary expense like home repairs or medical bills. Your lifestyle can play an important role too. Consider how long you’d need funds if your job suddenly disappeared and plan accordingly. How to Survive in a Cashless Society

Of course, the financial situation in any given family is different. The guidelines for the amount of money required would need to be adjusted based on family size and desired minimal lifestyle. Another consideration is the unique need for medication for sick or older people. Only you know if there are any other factors to take into account.

Budgeting Tips

Having enough money available for basic necessities such as food, rent/mortgage payments, and utilities during emergencies should obviously be factored in. Don’t forget about discretionary spending either! Experts suggest including some allowance for entertainment and personal care items like haircuts/manicures etc. You don’t want these things to become stressors during tough times.

Setting up automatic transfers from checking accounts into savings accounts may also be useful. By regularly depositing funds from each paycheck into savings, you can still allocate portions towards immediate needs. You still have the flexibility of investing any remainder in other areas such as stocks/equities.

At the end of the day, building up an adequate emergency fund requires planning ahead and creating achievable goals. Doing so will help protect against financial crises down the line if life throws unexpected hurdles our way! 8 Paramount Lessons Budgeting Has Taught Me

How much money to have available in an emergency fund?

A safety net is important because when a true emergency takes place, having a reasonable amount of cash on hand is vital! Having large amounts of cash around can be risky due to theft, fire, floods, and more. We’ve always had a small fire-resistant safe in our home to hold some cash made up of smaller bills. We also stored some valuables and critical documents we may need like insurance policy info, passports, birth certificates, etc.

I’ve suggested to my readers to shy away from storing larger bills in their safe or emergency kit. Many establishments won’t accept large bills, particularly if you’re expecting change back from your purchases. You’ll see signs in some places that state they only accept $20’s or smaller and that that is the largest denomination in their own cash safes.

It’s important to factor in other sources of income when calculating your emergency funds such as investments, side hustles, inheritance, etc. This will allow you more wiggle room if you experience unplanned but necessary expenses like home repairs or medical bills. Additionally, your lifestyle plays a role in setting realistic goals for your emergency fund. Consider how long you’d need funds if your job suddenly vanished, and plan accordingly.

These funds aren’t designed to cover long-term needs but do need to be sufficient to cover some significant expenses that may unexpectedly arise.

Is it possible to hold onto too much cash?

Yes, it’s possible to hold onto too much cash. An emergency fund is important in case of unexpected expenses and other financial setbacks, but it’s important not to keep too much cash. This can cause you to miss out on potential gains from investments or other forms of growth. We all understand that there are diminishing returns for holding larger amounts of liquid assets without investing them.

It’s also a good idea to pay attention to interest rates for savings accounts and adjust your strategy accordingly if the rate changes significantly. You’ll know the right amount for you! You can make deposits into your cash stash and your emergency savings as needs change or you use some of the funds as planned.

Should I save cash for retirement savings?

Obviously, whatever you have extra cash for is up to you! As mentioned, a good rule of thumb is to have at least 3-6 months of emergency money put away. However, retirement is different. It’s hard to know what income level you’ll need when you retire compared to what you made and used when you were working. Retirement funds are important, but how much of that is physical cash is up to you! Just remember, these funds are designed for emergencies.

Should I pay off my credit card balance?

The answer is always yes! You save money down the road by paying your credit cards off. One of the easiest ways to save cash is to ensure you have those credit cars paid off. Credit card debt can be hard to manage, but stay focused on keeping your debt low. How to Deal with Inflation as a Prepper

Final Word

Now, you can have excess cash or a cash stash and feel more secure financially. Some people love the idea of having their money in a high-yield savings account. Just keep in mind that when an emergency hits, it may be very hard to find your debit cards and take money out of the ATM. Plus, some banks and ATMs will only allow you to take out a small amount. So, there’s nothing wrong with keeping a rainy day fund at home, stashed safely away!

If you have some additional ideas, I’d love to hear them so I can share what you know and have experienced with my many readers. May God Bless this world, Linda

To me, this topic means ‘how much actual currency should I keep in the house, ready for a quick getaway?’ And, being in the Texas Gulf Coast, the answer is $3000, all in mixed bills from $1 through $100. I have bundles of $1, $5, and $10, with $1000 in $100 and the balance in $20 and $50. I keep this in a canvas bag in my gun safe.

The $ amount was calculated to cover all costs incurred for a week by two people, assuming lodging can be found somewhere (we also have our 72-hr kits), with sufficient margin to make a major purchase if need be. Your mileage may vary.

Hi Tim, I LOVE LOVE LOVE your comment! This is exactly what everyone should be calculating, their own needs in case they must be evacuated. I remember growing up and my dad taught me you always keep a $20.00 bill hidden in your wallet in case of an emergency. Well, times have changed and that was many years ago. Great comment! Love it! Linda

Hello again.

Forgot to mention that I also keep $100 in small bills in the console of my Expedition as well as two rolls of quarters.

Last year, a neighbor down the street was moving and decided at the very last minute (the moving van was being loaded) that that they really didn’t want to take a huge sectional, which was almost new, since they were downsizing out of state. They offered it to my wife, who was there saying goodbye, for $500, and the movers said they’d bring it over and set it up upstairs in our media room for $150. Cash was needed, and very quickly, and so this is just yet another reason to keep an emergency cash stash on hand and ready accessible. Just BE SURE to replace what you take out of it, which of course I did.

Hi Tin, that was a sweet deal! Have to love that one! I totally agree with you on keeping small bills and quarters as well. You never know when you may need it! Linda

I think this is very important and overlooked. I know folks who have large funds of PMs but no cash. Even if it’s not SHTF things happen in regular life that often require emergency funds.

A few times I was able to use it for opportunities as well. A gun or ammo purchase that was an immediate “hey I gotta sell this so I can..” and I would do it based on needs.

Look right now at the gas lines out west and imagine what happens if the card readers stop working.

Hi Matt, great comment as always! The biggest fear was the gas stations running out of gas in California because panic was driven from LA to Las Vegas, Nevada (where the pipe was leaking). One more reason to keep your gas tanks topped off if possible. The card readers won’t work in a power outage but will also not work if the gas is depleted. I just read where the pipeline was repaired but the Governor did declare a State of Emergency when the leak started. Now gas is flowing safely again in Nevada and throughout Southern California. We must be ready for anything that comes our way. Linda

This is one area my husband and I completely agree on. We feel three months is a respectable amount although it depends on which three months we are talking about. We own our home and car outright, but our property taxes are due in October and February…..those can take a real bite out of any plan.

Our grandsons built up a good little nest egg by getting $100 a time in rolled dimes and going thru the rolls for the older dimes with the higher silver content…..scrap silver, I think they call it. The boys have discovered savings accounts and interest, which may not be much, but it is something. Most recently, we took a bag of Reese Peanut Butter Cups, and peeled the back seam just enough to slide in dollar bills, then resealed with clear tape. Our grandson will remember trying to figure out how we got it in, and he didn’t get another toy he didn’t need. Children are never too young to learn how to save. It will prepare them for whatever is about to come.

Hi Chris, oh I LOVE this comment! What a great way to teach kids to save money. Hard times are coming, although it seems pretty hard right now! The silver in dimes, I love it!! Linda

When you withdraw larger amounts of cash from the bank, save the withdrawal slips and store them with the cash. It proves that it is your money and was not ‘acquired’ by any surreptitious means. I remember the account of the college student who was driving cross country with his life savings of $10,000. He was pulled over for some reason, they searched the truck, and confiscated his cash. Pleading that it was all he had to live on for the next year was to no avail. He could not prove it was his and not drug money or some other nefarious gain. He eventually got it back, but it took a long time, lawyer, etc. Who needs that!? I realize you are storing it in the house, but you never know. Better to be safe.

Thanks for the great newsletter!

Hi Cynthia, oh my gosh, this is terrible! Oh my gosh, then he had to hire an attorney!! This crazy! I LOVE this comment about showing/keeping a receipt with the cash and maybe a duplicate in the glove box. You never know these days when you get pulled over. It’s really a shame what that college student had to go through. Better to be safe. Great comment, Linda

I had a nice little bundle of cash on hand then my truck needed fixing. I had to use it all and still had to borrow but it was so much less. Had to start my stach all over but was glad I had most of it on hand to pay that bill.

Hi June, I know, right? Every little bit adds up and when we need it, we need it. Glad you got your truck fixed!! Linda

I recall many times people saying if you kept cash at home that it could be stolen and was safer in a bank. Times have changed and presently if the crap hits the fan, I fear that banks will refuse to let people make withdrawals, so it is imperative to have some cash at home or somewhere that you can get to it.

Digital currency is like imaginary money. It’s recognized as yours, but it can be kept from you. You have no control over it if credit card companies, banks or whoever refuses to process transactions.

Again, I say have cash, but if we have supplies and prepare, we might be able to get by without depending on purchases. An emergency or crisis situation is not the best time to go shopping.

Hi Frank, oh you are so right if there is a disaster that is NOT the time to go shopping! You know it’s funny I was a banker for many years, and I always had a safe deposit box (free) because I worked there. But then the power went out one time and of course, the bank protocol is to lock all the doors. As I watched this, I realized for me anyway, that I would empty my safe deposit box the next day and purchase a heavy-duty safe for my home. I realized at a young age, the safe deposit boxes would be locked if we had a power grid outage. There is no way you can open that huge safe door without blowing a hole in it I guess. I have talked for years about ATMs or credit cards that will be useless if we lose power at stores, banks, gas stations, etc. We must be self reliant and do what is right for us. Linda

Linda,

Cynthia’s comment was pure gold. Jane and I had that very problem when she saved a large amount of cash over the course of many years and then tried to deposit it. Fortunately, our old bank in a different State still had the records we needed to prove it wasn’t “new” money.

Hi Ray, oh my gosh, I know about those forms to REPORT large deposits of cash. As I remember there was one for over $3000.00 and of course, another one for over $10,000.00. Some paperwork just bugged me. Linda

And starting this year the threshold is only $600, though the IRS is waiving that requirement for that part of 2022 when the law went into effect. It’s getting ridiculous.

Hi Ray, that’s good to know! Things are changing all the time! Crazy times!! Linda

The risk/benefits of cash can be a sticky subject. We manage our budget using a cash envelope system, so we always have cash around, but will it be enough since we rely on that for our frequent purchases (groceries, etc) and for our infrequent expenditures, like car repairs and camping trips. Plus what happens if the ATMs are down and we can’t get our weekly cash out? Our final decision was we did need some in addition to the envelopes. We have divided the cash into different places and purposes.

For our cars, we wanted some cash for when we needed it while away from home. For each car I put in $5 in quarters, 10 $1 bills, 2 $5, and 1 $10. Since then I’ve probably doubled all that and added a $100 in $20 bills. When I realized that all of us had dipped into this to use quarters in parking meters, I added a roll of quarters in a ziplock baggie to all our cars specifically for parking and tolls. Having the emergency cash in the car pointed out a shortcoming in our daily living planning. My oldest daughter and I have both used our cash for “emergency” stops at yardsales. While that is not an emergency, it is urgent and I’ve used that as a planning tool and keep extra cash in my car fund so that I can spend it for fun and needed items at yardsales.

We have cash in our 72 hour kits and if something happens and we have to leave home, we will also grab all our cash envelopes. In my area our biggest natural disasters would be blizzards and tornadoes. In the case of the first, we would shelter at home and wouldn’t need the cash. In the case of the 2nd, if we are hit by a tornado, it’s possible keeping cash at home would be of little or no help. If the house is destroyed, chances are slim that we will find our cash so it will really just be “cash gone.” At the same time there are other emergency situations where we might have to leave home and would need our cash to do so. I have enough to cover the two of us in a hotel for 3 nights, or if the weather is cooperative it will cover about a week camping. We would have enough for groceries in addition to our 72 hour food kit. Until recently, we had a fund that we jokingly called the “death fund” in case one of our parents died and one person would fly out while the other drove cross country with the kids. When my father passed away, it was decided that I would fly back but hubby and kids would stay home. Sadly both of our mothers passed during covid and we weren’t able to get home for their funerals. For any people with elderly parents this is something that needs to be planned for.

Interestingly, back in the middle of the pandemic I read an article that stated that every American family should have $2,000 in cash in addition to any emergency fund in case of a national disaster. It was an interesting article and I’m sorry I can’t find it now to share. I don’t know that it is necessary to have both an “on hand cash” fund plus a national disaster cash fund, I think one is enough.

Hi Topaz, I’m so sorry to hear about your mother and mother-in-law passing during Covid. Funerals are expensive. I see at least 5-10 “Go Funds Me” a week on social media. Utah has one of the highest suicide rate states in the US. It’s really sad, kids to 80 years old. Cash is so important no matter what it has to be used for. Life is fragile, Linda

Linda, For my mother, it just happened to be during COVID, she outlived my dad my almost a year, longer than any of us thought she would. For her, COVID didn’t change much. After our dad passed, Mom wanted to leave assisted living and come home. Really the only reason she was there was to keep her and Dad together. At the time both my sister’s were living in Mom’s house. My youngest sister’s daughter and family lived with them and her son and his family lived next door. Mom’s daily life included, 2 of her children, 2 grandchildren (and spouses) and 4 of her great-grandchildren. It was kind of a 2 household family bubble and a happy environment for my mother. Mom was 93 when she passed.

MIL was a different story, she had Alzheimer’s was in a nursing home during COVID and not allowed any visitors. When the nursing home realized she was dying at that time, they allowed only one family member to visit and when my BIL went in, he was told if he left for any reason, he could not return. It was so sad and lonely. MIL passed about a week before her 90th birthday.

It’s horrible about the suicide rate being so high in Utah. I looked up the states with highest suicide rates for 2022 and I was surprised to see Wyoming and Alaska as the top 2. I would have thought that the huge metro areas like NYC and Chicago would be up there. I wonder what is it that causes that in those 10 top states.

Hi Topaz, oh those Covid days were terrible. What a blessing that your mother was able to come home and live with family before she passed. We have had family members commit suicide and it’s rough. Friends as well. Mental health is worse than people may realize. You can talk to people about cancer treatments but mental health is a bit different. It makes me sad. Suicide will be much higher I the coming years, I’m afraid. I hope I’m wrong. Hug your family members, Linda

I keep $700 in my wallet mostly $100s . $500 in my bag, 10k in my safe . Nothing smaller than $20s but mostly $100s . In today’s climate what’s a $20 going to get you ? 4 gallons of gas ? It costs my wife and I $60 bucks for lunch out ,ok a couple drinks too .In a shtf I’ll out bid the next guy and not care one bit what it cost .

Hi Larry, you know you are so right, boy have expenses changed! We really do need to raise the bar in our stash of cash, great comment! I remember when gas for my car was $.29 cents a gallon. Yep, those were the good ole days! LOL! Linda

We keep cash in the car for hotels and gas, but most importantly we keep some clean crisp dollar bills in the car. This is all in addition to our 3 months of expenses safely in the house. The dollars are for emergency food at a vending machine. If you are traveling and everything stops, food could easily become a huge problem. Not very nutritious but keeping your belly full helps you to make wise/better decisions, and helps to minimize fatigue.

Hi Dave, oh I like this idea! You are so right if all we have to choose from is some vending machines those crisp dollar bills will be great! Love it! Linda

My dad passed away almost 11 years ago. Then, just around the time covid hit, my mom had major health issues and was put in a rehab facility for older people. I am an only child and was still working full time. Both of my daughters came to help out and then mom went into the rehab facility. Then covid hit. No one was allowed to visit. It devastated me. (all of us, actually) We spent that first Christmas standing in the cold rain, at her window with a phone talking to her. At least we could do that. When she was well enough to leave, I had to find her a foster care facility, as, again I was still working and I lived 30 minutes from the city and over an hour from a hospital. I cried every night thinking about putting her somewhere that she could very well die “alone” or that I could not visit her to make sure she was being well taken care of. God must have been listening, as we found her a wonderful foster home where the primary caregiver was SO wonderful to her. Mom even said she wanted never to be moved from this foster home. She was there for almost 4 years, and passed away after covid was ‘over’ One of the caregivers even came to the hospital where she died after never waking up when the “hospice people could not treat her in the foster home. I still get angry about that. Hospice care, the ONLY purpose of Hospice care is to manage pain. They stopped what the foster home was doing that WAS managing her pain, and then would not give her what DID. I still cry over the fact that I had to go against her wishes not to be removed from foster care to go into hospital. This was the DAY AFTER I SIGNED the papers for Hospice care. Both caregivers were also so very upset about it. Covid was TERRIBLE!!!

Hi Carol, oh my gosh, I can feel the anguish in your comment, the sadness of having to do what you did. I’m so sorry. Getting older is not what I had expected at all. I’m only 75 and my husband is 79. What a blessing for your mother in the foster home, God is good. Covid was terrible, in soooooo many ways. Linda